AMERICA IS EXPERIENCING A HOUSING AFFORDABILITY CRISIS

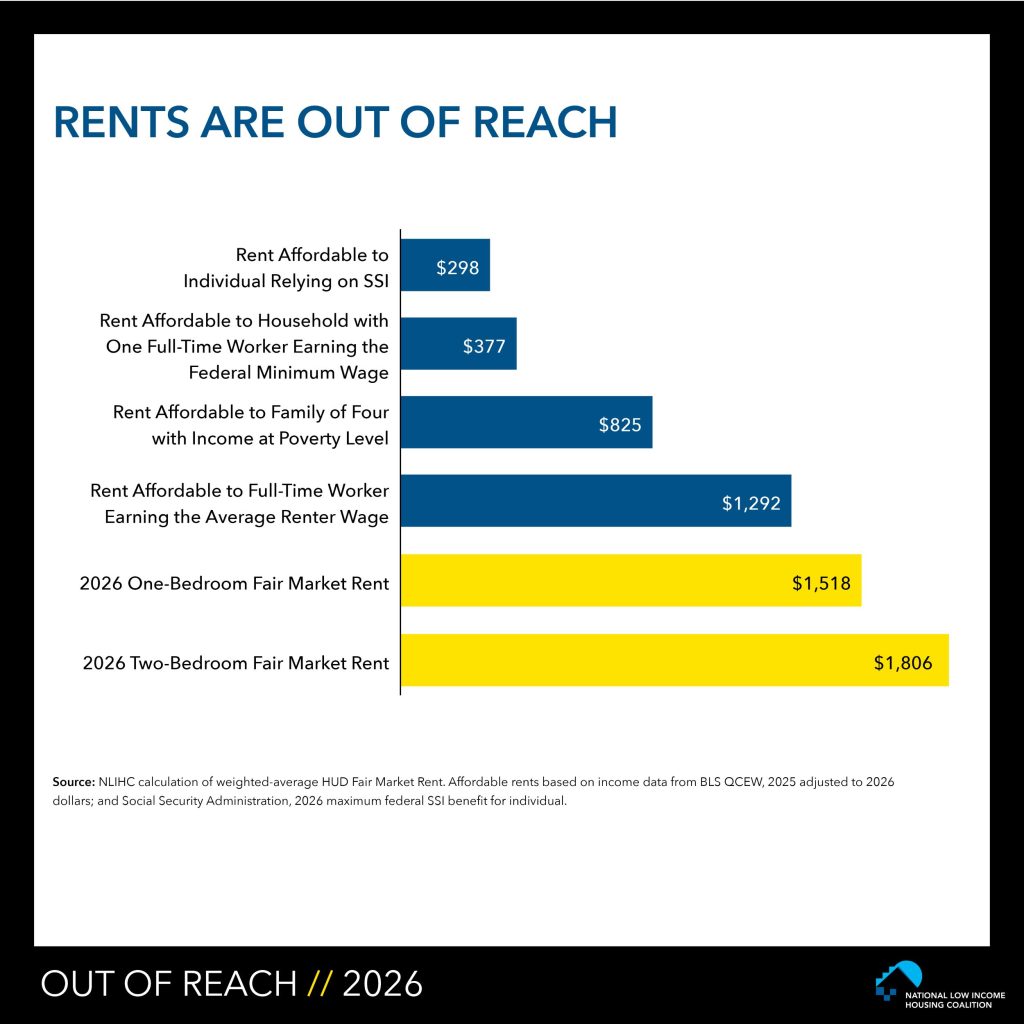

- “In 49 states, the District of Columbia and Puerto Rico, the average renter wage is not enough to afford a two-bedroom rental at fair market rent (FMR). In 36 states, it falls short of affording even a one-bedroom rental.” (NLIHC, 2026)

- The 2026 national Housing Wage is $34.73 per hour for a modest two-bedroom rental home, $27.48 higher than the federal minimum wage of $7.25 per hour. (NLIHC, 2025)

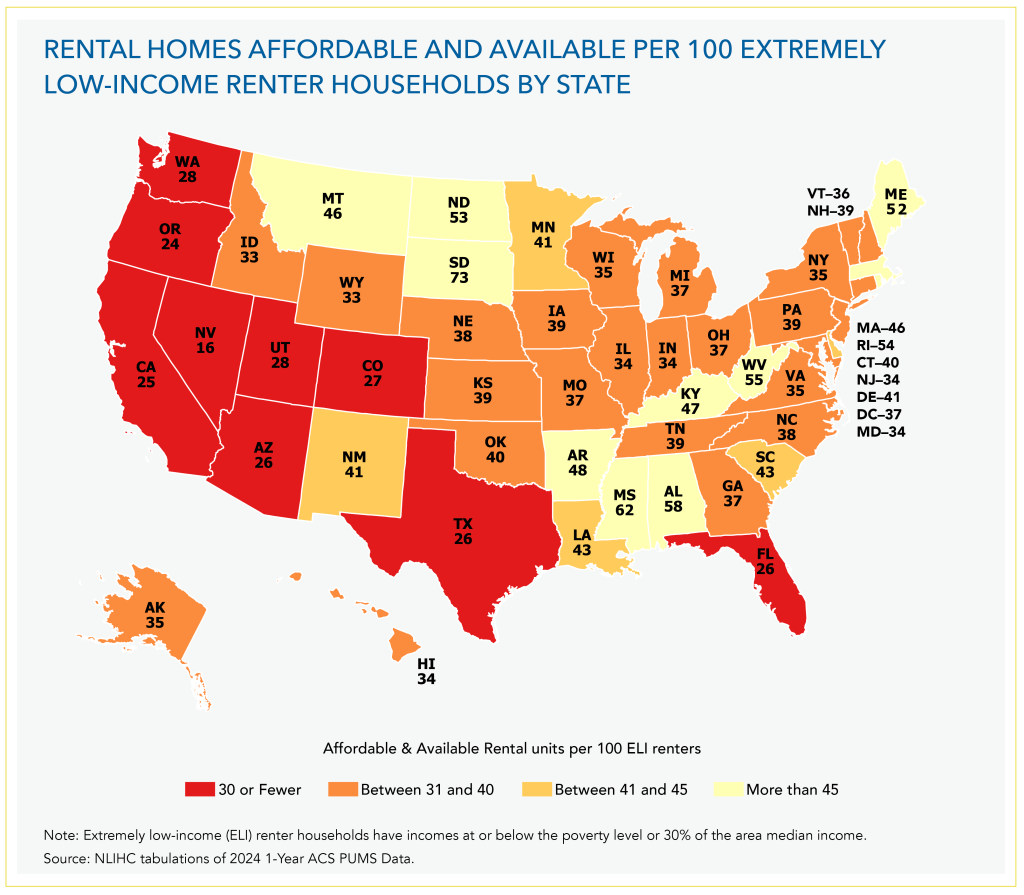

- Extremely low-income renters in the U.S. face a shortage of 7.2 million affordable and available rental homes. Only 35 affordable and available homes exist for every 100 extremely low-income renter households. Seventy-four percent (8.2 million) of the nation’s 11 million extremely low-income renter households are severely housing cost-burdened, spending more than half of their incomes on rent and utilities. Many are forced to make impossible choices between shelter and food, healthcare, education, and other basic needs. (NLIHC, 2026).

- The number of households with “worst-case housing needs” – that is, households with very low incomes that either pay more than half their income for rent or live in severely substandard housing, and receive no aid – reached a new high in 2021 with 8.5 million renter households with worst case needs. This is an increase of 760,000 cases compared with 7.77 million in 2019, and the 2021 count of households with worst case needs is the highest ever recorded (HUD, 2023).

“Black, Latino, and American Indian or Alaska Native (AIAN) households are

“Black, Latino, and American Indian or Alaska Native (AIAN) households are

disproportionately extremely low-income renters and disproportionately impacted by

the housing shortage. Eighteen percent of Black non-Latino households, 16% of AIAN

households, and 13% of Latino households are extremely low-income renters compared to

just 6% of white households.”(NLIHC, 2026).- A lack of affordable housing drives homelessness. People become homeless when they cannot afford a place to live. Because of a history of discrimination, people of color are most acutely impacted by the housing affordability crisis and are therefore more likely to experience homelessness. For example, 59 out of every 10,000 Black residents in the U.S. experienced homelessness in 2023, compared to 15 out of every 10,000 white residents (NAEH, 2024).

- “Of the 25 most common jobs in the U.S., 17 pay median wages below the Housing Wage for a one-bedroom rental, and 18 pay below the Housing Wage for a two-bedroom rental. These 18 occupations employ about 74 million people, 48% of the workforce.” (NLIHC, 2026).

UNAFFORDABLE HOMES DRIVE PEOPLE WITH LOW INCOMES DEEPER INTO POVERTY, DEPRIVE THEM OF OTHER NECESSITIES, AND LIMIT THEIR CHANCES OF CLIMBING OUT OF POVERTY

- A lack of affordable housing leaves households without enough money left over to afford necessities. According to the Harvard Joint Center for Housing Studies, severely cost-burdened (spending 50% of more of their income on housing costs each month) low-income renter households spent 50% less on healthcare, 48% less on food, 47% less on transportation, and 38% less on retirement than unburdened households in 2023.

- When families struggle to pay rent, they face greater risks of instability, eviction, and even homelessness, which research links to food insecurity, poor health, lower cognitive scores and academic achievement, and more frequent foster care placement among children (see sector pages for more detail on the multi-sector impacts on unaffordable housing)

- In a recent national opinion poll, 60% of respondents – including 52% of those living in rural areas – said that housing affordability is a problem where they live. A similar number (59%) of respondents said that the amount they pay for housing was a concern, with the heaviest burdens falling on individuals with low incomes, African-Americans, Hispanics, and renters (36%). To make matters worse, 2 in 3 (67%) respondents believe that the average cost of rent in the area where they live will increase in the next year, with only 2% expecting a decline. Nearly half (49%) of the public reports that they have had to make at least one sacrifice since the beginning of the coronavirus outbreak to make sure they can pay their rent or mortgage, such as cutting back on healthy food, stopping retirement savings, using a credit card, and skipping medical treatments to help cover all or some of their housing costs. (The Tarrance Group, 2021)

FEDERAL HOUSING ASSISTANCE SUPPORTS SENIORS, FAMILIES, AND OTHERS BUT IT IS CHRONICALLY UNDERFUNDED and POORLY MATCHED TO NEED

- 10.1 million people in 5.2 million American households use federal rental assistance to afford modest housing. 69% are seniors, children, or people with disabilities. But 4 in 10 low-income people in the United States are experiencing homelessness or pay over half their income for rent. Most don’t receive federal rental assistance due to limited funding. (Center on Budget and Policy Priorities, 2025).

- Rental assistance lifts more than 2.4 million people above the poverty line. (Center on Budget and Policy Priorities, 2022)

- “One study found that universal rental assistance would lift over 7 million people above the poverty line and cut poverty rates by 29 percent for Latine people, by nearly one-fifth for Black, Asian, and Pacific Islander peoples, and by 11 percent for American Indians and Alaska Natives.” (Center on Budget and Policy Priorities, 2024).

- “Housing vouchers sharply reduce homelessness, overcrowding, and housing instability. And because stable housing is crucial to many other aspects of a family’s life, those same studies show numerous additional benefits to vouchers. Children in families with vouchers are less likely to be placed in foster care, switch schools less frequently, experience fewer sleep disruptions and behavioral problems, and are likelier to exhibit positive social behaviors such as offering to help others or treating younger children kindly. Among adults in these families, vouchers reduce rates of domestic violence, drug and alcohol misuse, and psychological distress.” (Center on Budget and Policy Priorities, 2024).

- Rental assistance enables families to live in safe neighborhoods with quality schools, which improves children’s chances of attending college and earning significantly more as adults. (Chetty 2015)

- Federal housing expenditures are poorly matched to need and overwhelmingly benefit homeowners, not renters in need (Center on Budget and Policy Priorities)

- “Funding for affordable housing solutions has been declining for decades. Adjusting for inflation, the federal budget authority for housing assistance programs in the 1970s was nearly three times more than it is today, despite the significant growth in the number of low-income renters eligible for housing assistance.” (Diane Yentel, Testimony to House Financial Services Committee, 2019).

A large-scale, sustained national commitment is the solution

Failures of both the private market and public policy — at the federal, state, and local levels — have contributed to today’s housing crisis. And many people and institutions, both private and public, must take part in addressing it. Among these institutions, the federal government has an indispensable role to play. The Opportunity Starts at Home campaign has outlined a set of federal policies that we believe are necessary to solve the affordable housing crisis facing the poorest individuals and families.

Federal action is necessary not only to expand resources, but also to set overarching policy priorities and incentivize and support coordinated efforts at the state and local levels. While state and localities also have important roles to play, they cannot solve this problem on their own.

Federal action is necessary not only to expand resources, but also to set overarching policy priorities and incentivize and support coordinated efforts at the state and local levels. While state and localities also have important roles to play, they cannot solve this problem on their own.

Click here to read the campaign’s National Policy Agenda, entitled “Within Reach,” which outlines three key policy strategies: 1) bridging the gap between rents and income through rental assistance; 2) expanding the stock of housing affordable to low-income households; and 3) stabilizing households by providing emergency assistance to avert housing instability and homelessness.